What are Pilot Trusts?

A Pilot trust is set up during the lifetime of an individual in order to receive funds and/or property upon their death from a legacy in their Will, a pension fund, a life insurance payout or a death-in-service benefit. Also known as feeder trusts or family bypass trusts, they are normally discretionary and can be created with as little as one pound in the original trust document.

Taxation of trusts

The changes to the taxation of lifetime trusts proposed in last year’s Budget, but postponed in the Autumn Statement, have now been resolutely kicked into touch. The Chancellor has confirmed that the proposed to introduce a so-called ‘settlement nil rate band’, which would be spread across all lifetime trusts created by the same settlor, will not now be introduced.

However, the Government will still pursue ways of reducing tax avoidance through the use of multiple trusts (so-called ‘Rysaffe planning’). The details on this are to follow, but it has been confirmed that:

- The rules will only apply to additions to more than one relevant property trust made on the same day

- There will be a de minimis of £5,000 (i.e. additions of £5,000 or less will not be treated as a same day addition – allowing for additions to cover trustee fees, for example)

- The calculations will be simplified so that non-relevant property will not have to be included in the calculation of the relevant property charges (i.e. ten-year anniversary charges and exit charges)

- The grace period for additions to existing will trusts where the will was executed before 10 December 2014 will be extended to included deaths occurring before 6 April 2017.

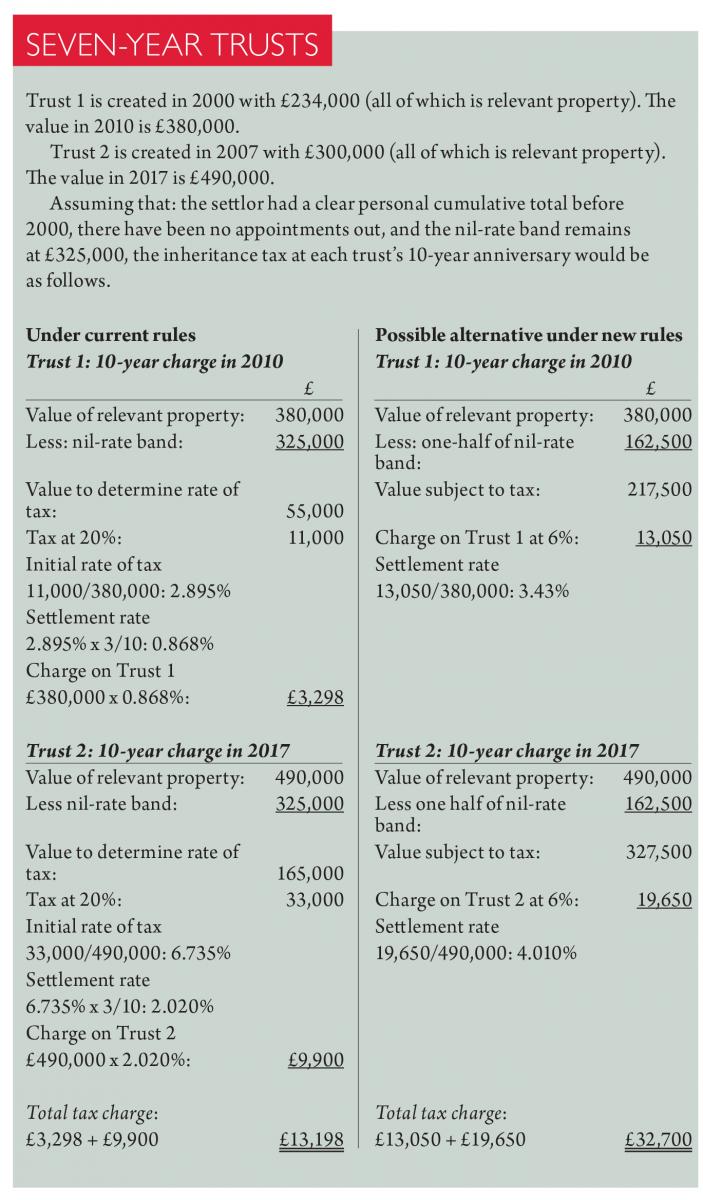

HMRC’s 7 year Trusts Proposal

Potential Impact

The potential impact is simple: where settlors have more than one relevant property trust, the trusts could end up paying more inheritance tax under these proposals.

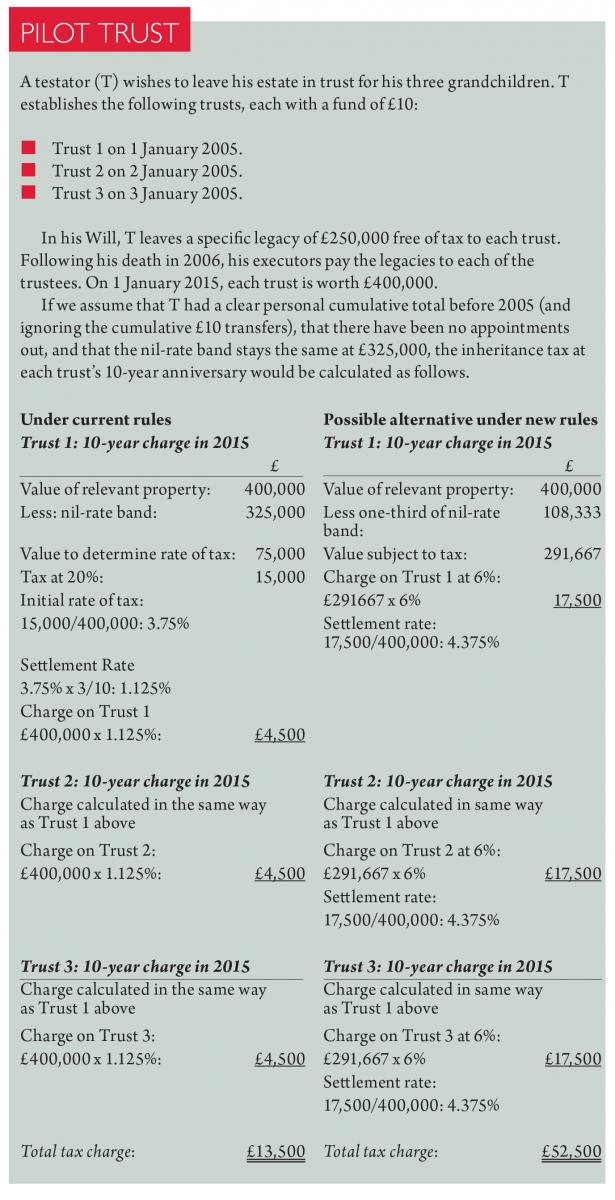

Pilot Trusts

A similar situation arises with pilot trusts. The examples given by HMRC in the May consultation ignore this type of tax planning, but if the proposed new rules are applied to a typical pilot trust arrangement, the outcome is likely to be far from tax neutral.

The inheritance tax treatment of pilot trusts was confirmed in Rysaffe Trustee Co (CI) v CIR [2003] STC 536.

Pilot Trusts by HMRC

Furthermore, part D26 of HMRC’s GAAR Guidance states that HMRC accepts pilot trusts as a long-established tax planning practice and they are not regarded as abusive for the purposes of the GAAR.

Conclusion

If you need have any concerns on the process or require further information please contact us.

If you want to read more about the various topics and services we provide, then please go through our FAQs.